The Ft Issue: Liquidity Crunch

Last week, Franklin Templeton (FT) AMC announced winding up of six debt schemes as these schemes faced unprecedented liquidity crunch mainly arising from rising redemption pressure amid the Covid-19 crisis. The fund house will be paying the investors as and when the securities in these funds mature and are able to recover the same from the issuers.

This has impacted their funds across tenors – including an ultra-short-term fund, which is usually considered as a safe instrument by investors for managing short term cash surplus, including treasuries of companies, both large and small.

What can be done for investors who are already in these funds? Nothing. But those who are yet to decide where do they go from here can opt for the best mutual fund distributor software to get past the present crisis that they are in.

First Level Ripple Effect

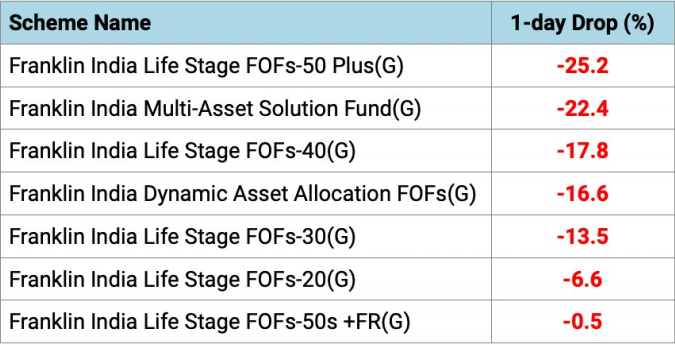

FT has a series of Fund of Funds (FoF) viz. Dynamic Asset Allocation Fund, Multi-Asset Fund and a series called Life Stage Fund of Funds.

The Life Stage FoFs has an inbuilt asset allocation model based on the age of the investor, which then invests into underlying FT equity and debt schemes.

These are specifically targeted for retail investors, especially through SIPs. Since conventional logic says that the higher the age, the higher the % age of Fixed Income, the 50s Plus FoF has the highest allocation to Fixed Income.

As a result of the 6 FT funds being wound up, the NAVs of these FoFs which included any of these funds, were also promptly written down. Considering for illiquidity discount, the fund house has marked down 50% of the exposure in FoFs having allocation to any of these 6 funds.

The NAV drop for most of these funds have been significant:

Returns as on April 24, 2020; Source: ACE MF

Second Level Effect

Bond yields moved up across the tenors (higher yield is lower price) as selling intensified on account of risk aversion and AMCs creating liquidity in their portfolio to meet redemption pressures.

The 3-year AAA Bond papers moved up by 25-30 bps and 10-yr Government securities inched up by 10 bps. These movements adversely impacted fixed income funds across the board and NAV movements reflected the same.

To ease the pressure on MFs, RBI has provided a liquidity window, of up to ₹ 50,000 Cr so that MFs can borrow at low rates and meet the redemption pressure.

Third Level Effect

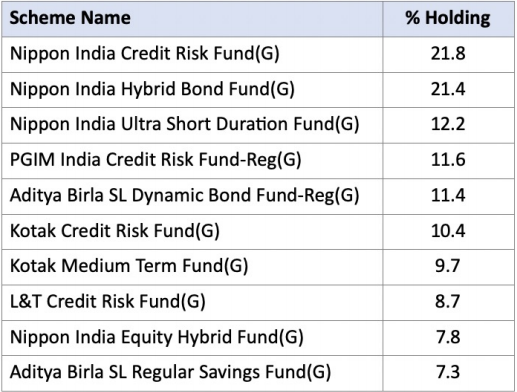

Mark-down or repricing of bonds and CPs of the same issuers would happen across the board for other AMCs. Even if there is no immediate pressure on the companies that issued the bond, the fact that FT would be a “seller” of these bonds would put untoward pressure on the issued bonds of these companies.

Based on the latest portfolio available, the following funds have an exposure to same promoters as that with the 6 FT funds (only issuers with A+ & below ratings are considered):

Top 10 schemes with overlapping promoter exposure with the 6 FT

Source: ACE MF, Fintso Research

Fourth Level Effect

For majority of the categories in the mutual fund space, the classification is based on the tenor of the underlying and not on the underlying quality of paper.

Given this issue, it is very likely that there will be changes announced in classification in terms of underlying paper and rating.

Re-classification will involve a certain amount of churn in the portfolio, and if the economic conditions are averse, fund managers would have to sell these securities at a lower price, thereby resulting in a drop in NAV.

What should you do?

1. Review each of your client’s fixed income portfolio

2. Re-evaluate their asset allocation giving a higher risk to fixed income schemes

3. Replace uncertainty with some stability – including Quality FDs/Sovereign Gold Bonds

4. Monitor for exit opportunities, even if one needs to take a penalty on exit load & tax implication, the decision might be worthy of consideration

Meet the Investment Team :

Rajan Pathak

Co-Founder and MD

Rajan was a member of team who launched India’s 1st Multi-Manager and Fund of Funds AMC concept in India. He had also launched India’s 1st Multi Asset, Multi Product “WRAP” Accounts with online action capabilities. These WRAP accounts were Ranked with a 4 Star by Value Research for process and performance. With more than 2 decades of experience in financial markets, Rajan’s accomplishments include establishing successful B2B businesses supporting the financial entrepreneurs. His vast experience & deep understanding of advisor’s need help us build a strong framework of actionable insights.

George Mitra

Co-Founder & CEO

George was part of the Investment Committee and has been instrumental in designing the algorithms for products and advisory in his previous firm. George had helped design the Financial planning software and created the models for Asset Allocation using Efficient frontiers way back in ’00 while in Deutsche Bank. With over 25 years working with Ultra-HNI clients, George has a deep understanding on designing solutions for the end clients.

Kumarpal Jain

Head – 3rd Party products

Over the past 8-years in financial markets, Kumar has developed an intrinsic understanding on different asset classes and built an excellent product knowledge. This in-depth knowledge on markets and products would help us bring best of the advisory to investors to facilitate informed investment decisions. He was a core member of the team that helped create the processes that were used for Fund selection in both his previous organizations.

Follow us on

Website: https://www.fintso.com

Linkedin: https://www.linkedin.com/company/fintso

Disclaimer

The information herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been prepared based on public available information, internally developed data and other sources believed to be reliable. The directors, employees, affiliates or representatives (“entities & their affiliates”) do not assume any responsibility for, or warrant the accuracy,completeness, adequacy and reliability of such information. Recipients of this information are advised to rely on their own analysis, interpretations & investigations.

Certain statements made in this presentation may not be based on historical information or facts and may be “Forward Looking Statements“ including those relating to general business plans and strategy, future financial condition and growth prospects, and future developments in industries and competitive and regulatory environments. Although the Company believes that the expectations reflected in such Forward Looking Statements are reasonable, they do involve a number of assumptions, risks and uncertainties.

Readers are also advised to seek independent professional advice to arrive at an informed investment decision. Entities & their affiliates including persons involved in the preparation or issuance of this material shall not be liable in any way for direct, indirect, special, incidental, consequential, punitive or exemplary damages,including on account of the lost profits arising from the information contained in this material. Recipient alone shall be fully responsible for any decision taken based on this document.