Understanding the Impact of COVID-19 on the Investor Eco-System

In order to estimate the impact on the eco-system, it is important that we first understand the time period of the impact – i.e. by what time do we expect to get back to “normal” and the various players of the eco-system.

Let’s examine this from the view point of the various players: Clients, Regulators, Distributors and Manufacturers.

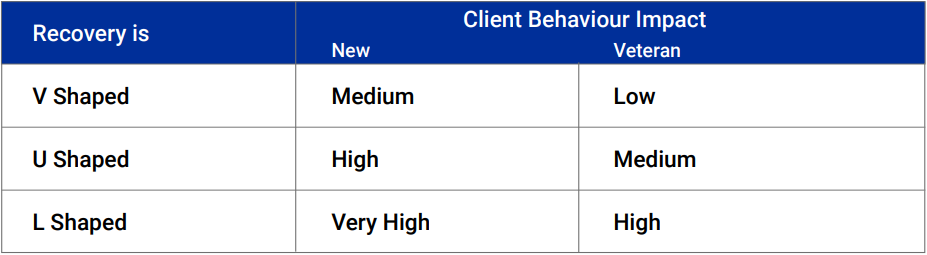

Client Behaviour

Essentially, if people expect a V shape “recovery”, habits and behaviour do not change much, and people “bide” their time before they go back to the way things were. However, if they think that it will be an L Shaped recovery, habits might get disrupted, which will have far reaching impact.

To illustrate in a simple way, a downturn in the equity market does not necessarily change investing behaviour, as long as people believe that it will go up.

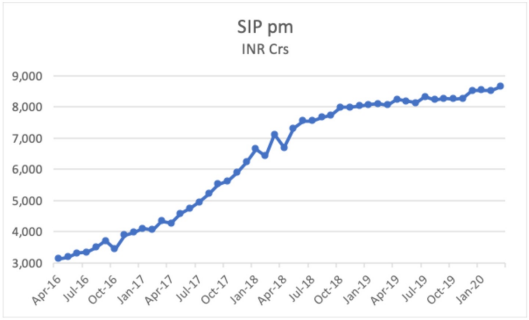

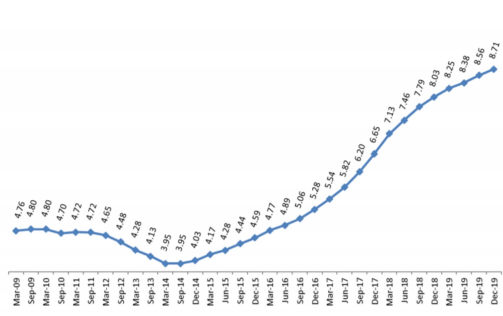

Investing into Equity through “Systematic Investment Plans” (SIP) is one such example.

SIP Growth has been the single largest factor for the growth of Equity Mutual Fund AUM of Individuals.

Source: AMFI

This is a growth from ₹ 3,100 Cr in April ’16 to over ₹ 8,600 Cr in March '20.

Monthly Inflow had shown a growth over the last financial year and was ~ ₹ 8,600 Cr despite the fall in the markets.

Cumulatively, it accounts for ₹ 2.39 Lakh Cr of AUM. The total number of SIP accounts were 3.12 Cr.

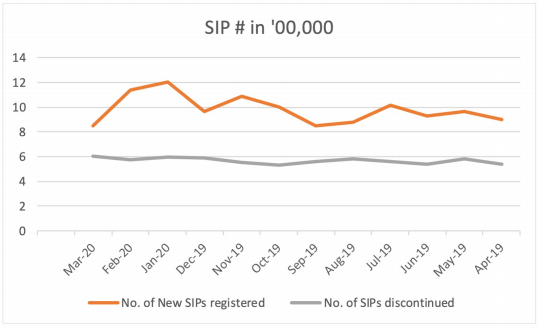

However, the data also shows that there is a constant need to register new SIPs in order to compensate for the discontinued SIPs.

Another dimension of change would be whether the Investor is “new” to the system or a “veteran”.

Given that the lockdown was only for a limited period in March, the actual figures for April, specially on the number of SIPs that are “discontinued” will be one of the factors that we need to follow closely.

Regulatory Changes

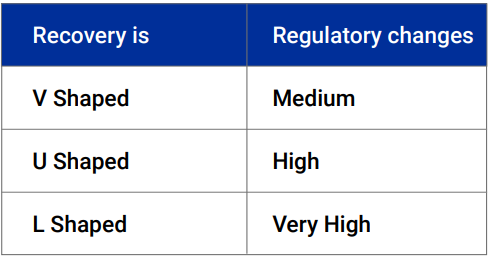

The next aspect to see would be on changes that may happen in the regulatory / structural environment.

There are changes that are done for the immediate needs: e.g. Moratorium on loans (will affect a LOT of lenders, including P2P), and some like the SEBI regulations that basically banned the usage of Papers for MF transactions.

The needs are immediate, and have an impact on business, but people don’t change their business models if they expect a V shaped recovery.

E.g. Distributors will not convert over-night to a digital platform if they think this is a temporary measure.

A longer impact, however, ceases to be a stimulus / reaction, and becomes a regulation and then a structural change. Such changes do result in business changes.

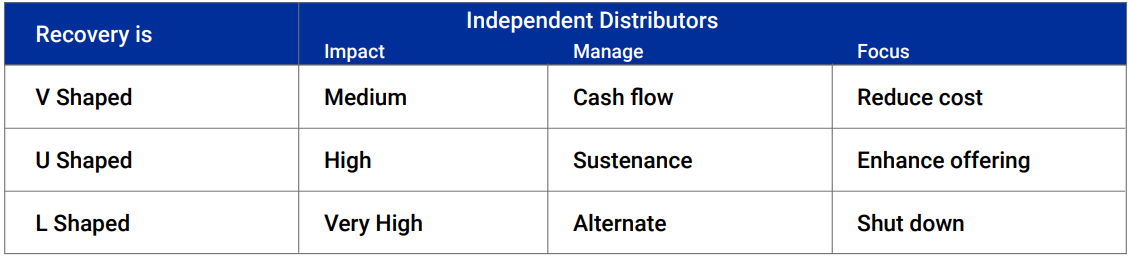

Distribution Eco-System

The impact that this will have on the distributors will be the biggest factor that will change the investor landscape.

The highly fragmented investor base in India – across needs (Retail / HNI / UHNI), geography and behaviour – and the importance of the distribution community is explained in the Annexure.

Note:

Cash Flow effect means that there could be revenue disruptions (new investments falling, redemptions, etc.) while establishment costs do not come down – e.g. rental and people costs.Sustenance: Business continuity is affected. To think of other lines of business, or to cater to other niche segments of clients needs – e.g. move from distributing MFs to actively distributing FDs and Health Insurance. Alternate: To look at consolidation – reduce branches. Seek active M&A for economies of scale.

This is perhaps easier to understand if we consider that each Independent financial entrepreneur – whether they are distributing MFs, or Insurance, or FDs, or helping an investor secure a housing loan, is a Businessman. They depend on selling services and solutions to sustain themselves.

While larger firms can sustain themselves due to historical business, the smaller players would be deeply impacted.

First, from a cash flow perspective – then from a sustainability perspective, if the recovery is not a V.

By their very nature, they depend on the close relationship that have forged with their clients and be their “bridge of trust” on decisions regarding finances.

This Means They Must Re-Invent:

· The way they communicate, embrace new channels of communication, including VCs, WhatsApp / Telegram, and email, but mostly importantly, their own digital App

· What they communicate – from a product sales pitch to solutions. Financial planning, portfolio construction and even ways to lower their costs (e.g. switching housing loans)

· How they monitor investments, reacting to risk more nimbly than they had to earlier

· Who they cater to – Rather than focussing on new client acquisition, consolidating their base, increasing the share-of-wallet from their existing clients by showcasing a wider bouquet of products and services? E.g. an MF Distributor may actively advise a client to take more health insurance as part of their financial plan.

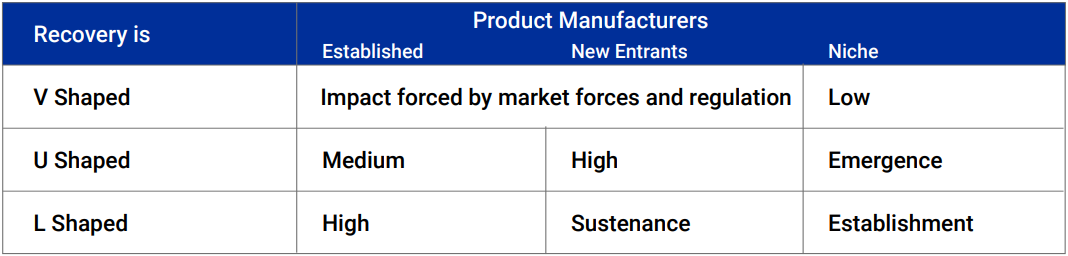

Product Manufacturers

If we divide this into three parts, Established players (MFs / Large PMSes, etc.), New Entrants (Boutique AMCs, AIFs) and Exotic (which cater to niche – e.g. LRS Offshore), the effect is going to be quite varied.

The change to paperless transactions may affect transactions and inflows in the short term until distributors adapt.

The wiping away of returns, even through SIPs, will result in a re-evaluation by the recent / new investors. The ability to survive and adapt will be the key to how these layers would emerge.

The “niche”, both existing, and new categories, will soon emerge – who are “native” to the new realities, who will find a niche just because they are relevant to the new “new”.

An example of this could be the LRS Funds – which would allow diversification OUT of the country as well as their ability to seek and invest into ideas beyond our borders. E.g. a specific WFH ETF (“Work-From-Home” Exchange Traded Fund) that is being launched in the US.

Effect on Distributors

Going by the latest pandemic situation it is safe to assume that we all need to embrace the digital method. Therefore, adapting to digital technology would not be an option anymore, it would become the norm. Besides with the growth of the MF distributor software and the emergence of the best financial adviser back office systems it will be a boon everyone including the distributors. Furthermore, they will also be benefited with:

First: Cost Reduction

To reduce Mid-office and Back-office costs by using automation for doing as much of the activities as possible, from engagement to execution to monitoring.

Embracing the concept of “shared economy” – of subscribing rather than buying / making on their own.

Second: Omni Offering

There will need to be a growth in the range of the product basket that each distributor would need to embrace.

The ability to effectively identify, tie-up, execute and monitor from the same platform seamlessly.

To become the one-stop-shop for all their client needs

Third: Create, Amplify and Defend their own Brand

The ability to create a differentiation, unique offerings and seamless experience, under their own brand, to cement the “bridge of trust” tag will become more important.

This will reduce the effectiveness of “aggregator” broker / sub-broker models.

Going Forward

We would continue this article with more data in May.

March only had a limited period of the lockdown, and the effect of the same has not reflected fully in the numbers available as of now.

April data on FDs, Mutual Fund Transactions, SIPs, Insurance, would be out by mid-May and a thorough analysis would give us an inkling on what the eco-system (Clients, Distributors and Manufacturers) are expecting – a V, U or L.

Annexure: Understanding The Indian Investor Base

Data at a granular level is extremely difficult to source, especially on a near real-time basis

Mutual Funds, even though the penetration is still small, is a proxy for looking at trends.

Number of “Investor accounts”

*Source: AMFI

Since Dec 2014 – Dec 2019, there was an increase from 4.03 Cr to 8.71 Cr investor accounts.

Of this, ~ 90% (7.80 Cr) belong to Retail investors (defined as investing < ₹ 2 lakhs)

Overall, Equity Oriented Schemes account for ~ 72% of this, and Hybrid Schemes for 11%

Individual investors grew by 15% YoY (Feb 19 – Feb 20) and was at ₹ 14.9 Lakh Cr. Equity Assets grew faster at 18% YoY.

Geographical Spread and Type of Assets

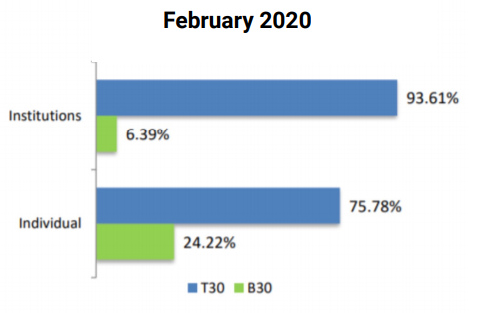

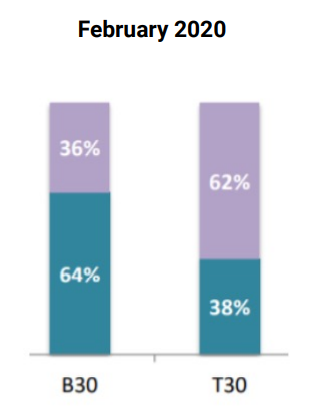

The Asset mix for B30 is 2/3rd Equity oriented – compared to T30 (reflecting the higher presence of Institutions in T30 16% of the Total Assets of MFs came from B30 locations: approximately ₹ 4.46 Lakh Cr is from B30 locations, of which the majority assets are by Individuals investors.

T30 = Top 30 Locations (metros and Tier I cities) B30 = Next 30 locations (includes Tier II and III)

Self Service (Direct) vs. Distribution Led

The Asset Type distribution shows that more complex products tend to be done through Distributors compared to self-directed investors. 81% of Equity Oriented schemes were under distributors.

Over 87% of Retail, and 78% of HNI invested through a distributor (both organised and un-organised).

Looking a little deeper into the mix:

Overall AUM distribution

Equity Oriented

In B30, Distributor AUM is 7X of Direct AUM - Overall and in Equity

From the above, we can understand the deep importance that the Distribution system has on Investors and investing patterns.

About Us

Fintso is a fintech platform that provides solutions to Financial entrepreneurs to address their needs, of research, advisory, product access and client engagement.

The team at Fintso has deep domain expertise on the Indian Investment space, Wealth management and cutting edge Technology.

Rajan Pathak

Co-Founder and MD

Rajan is known for his in-depth insight into the financial entrepreneur’s venture with 25+ years of establishing various B2B businesses, which gives him the edge and adeptness to scale the advisory business.

As the CEO of IFAN Finserv (formerly ING), Rajan managed a team of 40+ people, created a wide network serving 1300+ Independent Financial Advisors managing assets over $500 million.

He’s always on the move, this attitude comes from his passion as a trekker. He has a keen eye for photography and for vintage B&W classics.

George Mitra

Co-Founder & CEO

George has 22 years of experience in the Wealth Management space. As CEO, for Avendus Wealth Management, George was responsible for a 110-member team spread across 7 locations in India that managed clients’ assets worth $4 billion with a CAGR of over 60% over the last 5 years.

His rich experience in the financial domain renders him an expert in financial planning, product innovation, and advisory solutions.

His cooler side and his need for speed fuel his passion for super-sports biking, cycling and kickboxing beside being an expert and prolific scuba diver.

Follow us on

Website: https://www.fintso.com

Linkedin: https://www.linkedin.com/company/fintso

Telegram: https://t.me/fintso

Disclaimer

The information herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been prepared based on public available information, internally developed data and other sources believed to be reliable. The directors, employees, affiliates or representatives (“entities & their affiliates”) do not assume any responsibility for, or warrant the accuracy,completeness, adequacy and reliability of such information. Recipients of this information are advised to rely on their own analysis, interpretations & investigations.

Certain statements made in this presentation may not be based on historical information or facts and may be “Forward Looking Statements“ including those relating to general business plans and strategy, future financial condition and growth prospects, and future developments in industries and competitive and regulatory environments. Although the Company believes that the expectations reflected in such Forward Looking Statements are reasonable, they do involve a number of assumptions, risks and uncertainties.

Readers are also advised to seek independent professional advice to arrive at an informed investment decision. Entities & their affiliates including persons involved in the preparation or issuance of this material shall not be liable in any way for direct, indirect, special, incidental, consequential, punitive or exemplary damages,including on account of the lost profits arising from the information contained in this material. Recipient alone shall be fully responsible for any decision taken based on this document.