In the present environment, one of the things that has been at the top of everyone’s mind is the fragility of financial security – a loss of income (job loss and business loss), or an outflow (health being on top).

We do believe that just as we advise our clients on financial risks, it is also important to highlight and help them understand the risk protection mechanisms beyond financial investments - like Health Insurance.

Simply put, a health insurance covers a person against the risk of financial loss which may arise due to hospitalization. While we may have COVID-19 at the top of our minds, changing lifestyles and rising stress levels have exposed everyone to lifestyle diseases such as obesity, blood pressure, diabetes, and heart strokes. The high costs of treatment are compounded by double digit health care inflation rates which necessitates all of us to get sufficient health insurance cover.

A quick check on what clients normally do

Health coverage by Employer: Most salaried individuals have this. Key issues are around: Who all are covered as “family”? Are parents covered as dependents? How much is the coverage? And most important, what happens in the case of a job loss?

Individual health cover: When was this taken? Are all critical illnesses covered and from when does the coverage start? How much is the “co-pay”? Are all members covered though a “family floater”? Is the amount enough, especially if the policy was taken earlier?

Understanding the steps while recommending a plan for your client

Step 1 – Define your client’s need

We do believe that it is essential to be aware and informed of the best wealth management software in order to advise our clients properly. Furthermore, it is also important to highlight and help them understand the risk protection mechanisms beyond financial investments - like Health Insurance.

Step 2 – Choose the right insurance product or combination of products

Like any investment plan, having a combination of features is often more beneficial than a single standard policy. From the planning stage, create an ideal policy that will have the needed number of members, individual coverage, and a floating coverage, using top-ups that can be used to increase coverage without increasing the premium.

Step 3 – Select the right policy

Just as we do diligence for funds, we need to check what is covered and not covered under the policy.

Common Inclusions

- Inpatient hospitalisation benefits.

- Domiciliary hospitalisation

- Pre and post-hospitalisation expenses

- Road ambulance cover

- Day care procedures

- Organ donor expenses

- Health check-up benefits

Common Exclusions

- Waiting period of 30 days except for accident related emergencies

- Pre-existing disease cover after 24 to 48 months

- Any cosmetic surgery or dental surgery except accidental

- Any treatment arising from or traceable to pregnancy

- War, invasion, act of foreign enemies

- Intentional self-injury (including but not limited to the use or misuse of any intoxicating drugs or alcohol)

- Cost of spectacles, contact lenses, hearing aids, crutches, artificial limbs, dentures, artificial teeth

Insurance companies have also started providing the add-on benefits such as hospital cash, critical illness, maternity benefits, air ambulance, etc. on paying additional premium.

Step 4 – Get equipped to execute

Helping the client to execute on the solution is just as important as coming up with the ideal plan is.

It could be as simple as creating comparison charts with different options available, to getting an expert to re-validate the solution, to actually being able to initiate purchase of the policy for the client.

Conclusion

Getting equipped with the best financial adviser back office systems to do more for the client, to be able to address their most pressing needs, will help an Advisor become more relevant, and help strengthen their position of being the “Bridge of Trust” for their clients.

Illustrations & Ready Reckoner

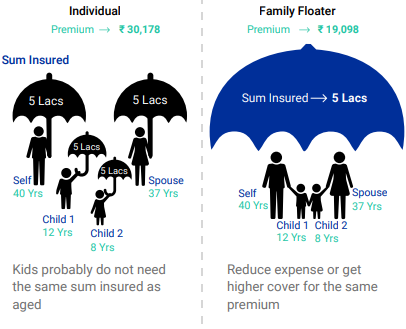

Benefits of Family Floater plans

Better than policies for each individual.

Risk: The only risk under family floater plans is when all the members fall sick or get hospitalized together. However, for the same premium, the higher sum insured still partially safeguards your client.

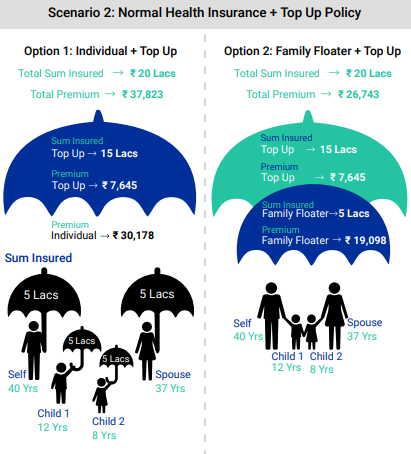

Benefits of Top-Ups

A top up can significantly enhance the sum insured without increasing the premium too much.

Choosing to go for a higher sum insured in the normal health policy leads to higher premiums:

Risk: The only risk under family floater plans is when all the members fall sick or get hospitalized together. However, for the same premium, the higher sum insured still partially safeguards your client.

Scenario 1 premiums are clearly higher than Scenario 2. However, let us understand the differences between the two options in Scenario 2.

If there is a claim of ₹ 4 lacs, the amount will be paid from the base policy, which means that the remaining ₹ 1 lac can be used for the next claim. If the claim amount is ₹ 8 lacs, ₹ 5 lacs will be paid from the base policy and ₹ 3 lacs from the top up policy.

Risk: If the base sum insured is exhausted in the first claim itself then other family members will be without any insurance cover as far as the base policy is concerned as the top up policy comes into picture only when the claim amount exceeds the base cover. Despite the risk, this is still a suitable option to get a higher cover at a reasonable cost.

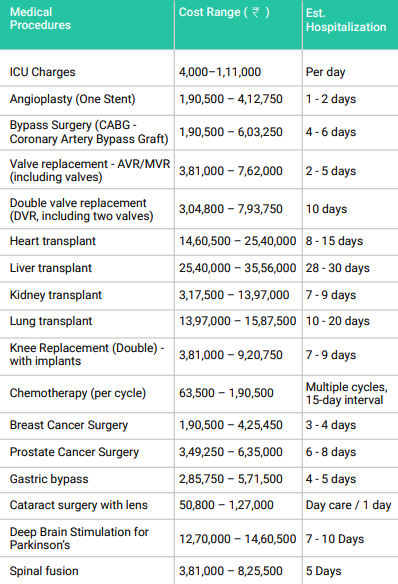

Expected Medical Costs in India

Conclusion

Each health insurance product has its own merits and demerits. Combinations of different insurance products can provide proper coverage,

- which takes care of normal hospitalization, incidental expenses,

- with an option to get an upfront amount to ensure a planned treatment for critical illnesses

- and a sum insured which shall be sufficient to take care of medical expenses in the current situation and the future inflation as well.

About us

Fintso is a fintech platform that provides solutions to financial entrepreneurs to address their needs of research, advisory, product access and client engagement. We empower entrepreneurs, to do more for their clients while retaining their identity.

The team at Fintso has deep domain expertise on the Indian investment and wealth management space and in cutting edge technology.

About the authors

Rajan Pathak

Co-Founder and MD

Rajan was a member of team who launched India’s 1st Mutli-Manager and Fund of Funds AMC concept in India. He had also launched India’s 1st Multi Asset, Multi Product “WRAP” Accounts with online action capabilities. These WRAP accounts were Ranked with a 4 Star by Value Research for process and performance. With more than 2 decades of experience in financial markets, Rajan’s accomplishments include establishing successful B2B businesses supporting the financial entrepreneurs. His vast experience & deep understanding of advisor’s need help us build a strong framework of actionable insights.

Chander Singh Chandel

Business Development

Chander is a Fellow of Insurance Institute of India (FIII) and has over 18 years of experience in financial services industry in retail business development with reputed organizations like RR, IFAN Finserv (Erstwhile ING) and SMC Global. As the Head of Business Development at IFAN Finserv, he served retails businesses through a B2B platform, expanded to newer geographies, and introduced new products such as corporate deposits and insurance on the platform.

Follow us on

Website: https://www.fintso.com

Linkedin: https://www.linkedin.com/company/fintso

Telegram: https://t.me/fintso

Contact us on

E-Mail: products@fintso.com

Phone: 022 4897 1500

Disclaimer

The information herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been prepared based on public available information, internally developed data and other sources believed to be reliable. The directors, employees, affiliates or representatives (“entities & their affiliates”) do not assume any responsibility for, or warrant the accuracy,completeness, adequacy and reliability of such information. Recipients of this information are advised to rely on their own analysis, interpretations & investigations.

Certain statements made in this presentation may not be based on historical information or facts and may be “Forward Looking Statements“ including those relating to general business plans and strategy, future financial condition and growth prospects, and future developments in industries and competitive and regulatory environments. Although the Company believes that the expectations reflected in such Forward Looking Statements are reasonable, they do involve a number of assumptions, risks and uncertainties.

Readers are also advised to seek independent professional advice to arrive at an informed investment decision. Entities & their affiliates including persons involved in the preparation or issuance of this material shall not be liable in any way for direct, indirect, special, incidental, consequential, punitive or exemplary damages,including on account of the lost profits arising from the information contained in this material. Recipient alone shall be fully responsible for any decision taken based on this document.