Using Machine Learning algorithm for tactical asset allocation

It is an endeavour of every investor to make money without taking any undue risk. This is the primary reason that we follow news, trends & advise (personal or professional) with an objective to interpret data so that we can make informed decisions and avoid pitfalls.

As our computers and smart phones constantly beep, flash and bombards us with information, it becomes extremely difficult for us to arrive at actionable insights on this data. Also, our own innate emotions, makes it even more difficult for us to take any action.

A case in point being, when the markets were falling and all the information we were getting in March 2020 amidst the outbreak of pandemic, would we have re-aligned our investment portfolios to go Overweight on Equities?

To use the vast amount of data and improve our investment making decisions, we explore the field of machine learning (ML), a subset of artificial intelligence (AI). At Fintso, we have developed a Tactical Intervention Approach (TIA) using machine learning which gives us the signal whether we should go overweight, underweight or neutral on equities.

Machine Learning and its evolution

ML enables powerful algorithms to analyse large data sets in order make predictions against defined goals. Instead of precisely following instructions coded by humans, these algorithms self-adjust through forward and backward propagation to produce increasingly more accurate predictions as more data comes in.

ML can potentially identify new patterns in large existing data sets.

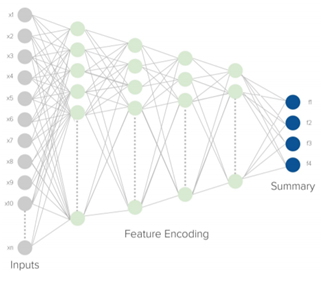

The Algorithm: The ML Neural Network has the following parts:

Summary: An answer to a specific question, or outcome, that we expect the program to answer

Feature encoding: The Neural network that we build out and “train” to interpret data. The endeavour is to recognize underlying relationships in a set of data through a process that mimics the way the human brain operates

Inputs: The set of data that we provide, which we believe may be of relevance

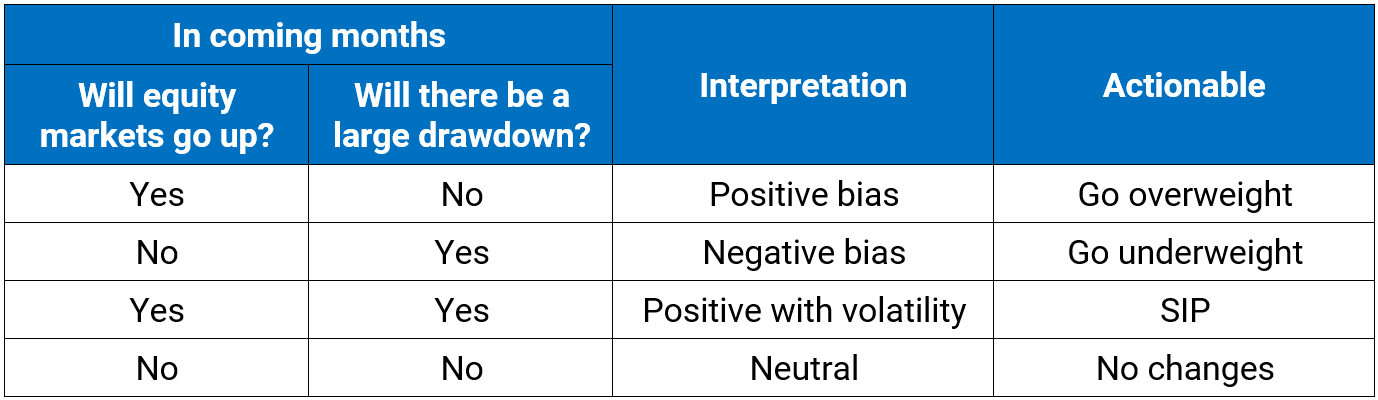

What Question did we ask?

Q1. Will the market go up significantly in the next two quarters?

Q2. Will the market have a big drawdown in the coming months?

The Output matrix for Action

We use the cash portion in the model portfolios (or fresh funds, if any) for implementing these tactical calls.

The Input parameters

We gave various distinct input factors to the machine, broadly classified into various categories such as macro (market capitalization to GDP), valuation (P/E, P/B, etc.), momentum indicators, trends, volatility, liquidity and so on.

The input factors considered are 15-18 unique parameters over the last 12-years. Besides their absolute value, we have taken the first derivative (implying % change and direction of the change) for some of the parameters. The sheer number of data points makes it difficult for a pattern recognition to be done by humans.

Training the Neural Network

Training the network involves a mechanism of providing the network with input data (training data) and the expected desired output. In our case, we would provide various historical input factors and desired tactical outcome. The input parameters pass through a series of layers with different combination of nodes to generate the desired outcome. The difference between the desired outcome and actual outcome is termed as error.

The network then propagates the error back through the system, causing the system to adjust the weights. This process occurs over and over as the weights are continually tweaked.

Once the network is trained, the same is tested on a set of different data (test data) to check the accuracy of the network. The above process is repeated several times till we reach an accuracy level of more than 80% in both our training and testing data set.

And what do the results show?

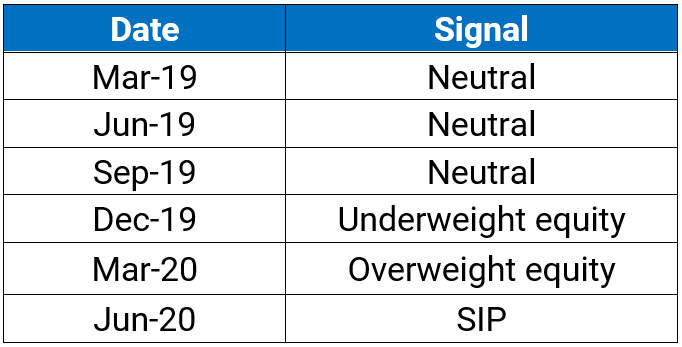

We used our ML algorithm from March 2019 till June 2020 and captured tactical calls on quarterly basis. The below table summarizes the same:

- Starting Jan 2020, the model suggested on reducing equity allocation and increase cash allocation

- Starting April 2020, the model suggested going overweight on equity

- Starting Jun 2020, the model suggested doing SIP (spreading any fresh investments across multiple tranches)

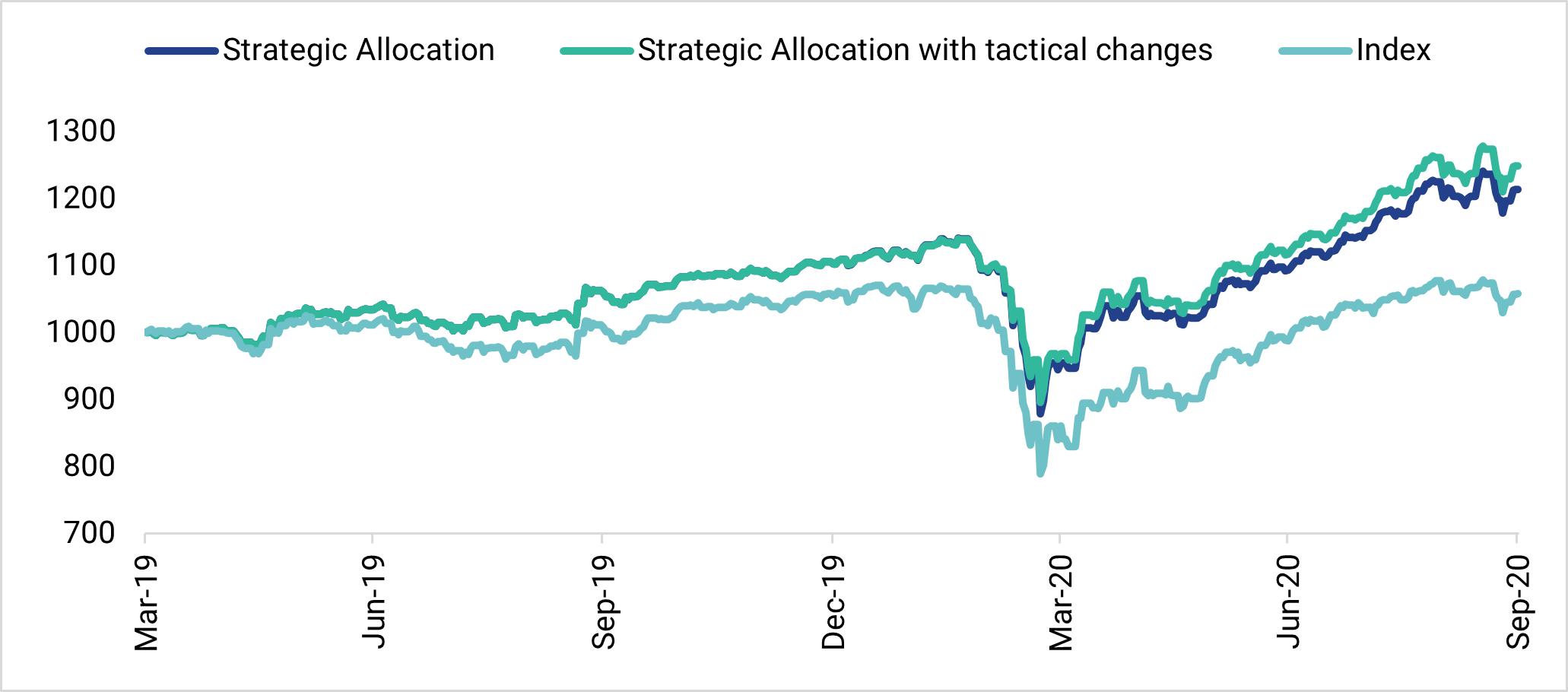

Based on the above signals, the performance of our Model Portfolio (for aggressive profile), with and without the Tactical Intervention, is given below:

The above changes in the model portfolio led to an alpha of 3.5% (from Mar 2019 to Sept 2020) over strategic portfolio. Strategic Portfolio itself had an alpha of around 15% overthe benchmark.

To recap our journey:

Stage 1: Create Model portfolios (strategic allocation) for different risk appetites using Mean Variance optimisation on 6 different asset classes including Gold and Foreign investments

Click here to know more about our Model portfolios.

Stage 2: Using our own algorithms to make Fund Selection for Equity Mutual Funds, which not only covers Quantitative measurements of Returns/Risk but also covers skill of the manager to manage the portfolio and his ability to take sectoral calls.

Click here to know more about our Ranking process.

Stage 3: Use ML to give active Tactical calls to enhance returns and lower risks

We believe our TIA shall significantly change the way we create investor portfolios, thereby helping the advisors to build a strong relationship with their clients based on long term value addition.

Authors

George Mitra

Kumarpal Jain

https://www.fintso.com/team